Applying sixth‑generation transmission technology to double speed

Reducing input/output latency and improving power efficiency

AI ecosystem shifts from training to inference‑centric

Proactively responding to the market as NAND’s importance rises

Samsung Electronics has begun mass production of next-generation high-performance enterprise solid-state drives (eSSDs – high-speed data storage devices using NAND flash memory) for artificial intelligence (AI) data center servers. As the center of gravity in the AI industry shifts from data “training” to real-time “inference,” the importance of high-performance storage devices (NAND flash) is growing, and the company aims to secure profitability by responding preemptively to demand in this market.

On the 8th, Samsung Electronics announced that it started mass production this month of the eSSD “PM1763” model equipped with the next-generation sixth-generation transmission technology (PCIe 6.0) interface. The product more than doubles bandwidth and data transfer speeds compared with existing fifth-generation (PCIe 5.0) products. Tailored to AI environments that must constantly read and write massive volumes of data, it minimizes data input/output latency and significantly improves power efficiency to reduce the operating costs of data centers, which consume enormous amounts of electricity. Earlier, at Nvidia’s annual developer conference “GTC 2026” held in March, Samsung revealed that this product is scheduled to be installed in Nvidia’s next-generation AI platform “Vera Rubin.”

High-performance eSSDs have recently emerged as a core market segment because the AI ecosystem is being reorganized around “inference.” In the inference phase, large-scale data must be supplied continuously and without delay to prevent any slowdown in computation speed. In response, Nvidia has also adopted the approach of installing high-capacity eSSDs in its next-generation AI systems to reduce data bottlenecks. This is the background to NAND, which was previously used merely for simple data storage, being re-evaluated as a high value-added specialized component that determines AI system performance, similar to high-bandwidth memory (HBM).

Although the role of high-performance NAND has expanded, the market is experiencing a severe supply-demand imbalance. As major memory semiconductor manufacturers concentrate their production capacity on HBM and high-capacity server DRAM, the volume of NAND wafers being processed has comparatively decreased. Meanwhile, demand is surging as large global cloud service providers (CSPs) such as Amazon Web Services (AWS) and Microsoft rush to lock in eSSD volumes through long-term contracts to ensure stable service operations.

With supply shortages coinciding with explosive demand, global NAND prices are tracing a steep upward trajectory. The price of general-purpose NAND, which stood at about USD 5.74 (approximately KRW 8,650) at the end of last year, had soared more than 400% to around USD 28.82 (approximately KRW 43,430) as of the end of June this year.

Amid the price surge, eSSDs have established themselves as a solid cash cow for semiconductor companies. In particular, eSSDs guarantee significantly higher margins than general NAND products, as they face high technological entry barriers and must pass stringent enterprise-grade quality certifications.

According to market research firm Omdia, global eSSD revenue is projected to grow more than six-fold in just one year, from USD 24.16 billion (approximately KRW 3.64091 trillion) in 2025 to USD 154.228 billion (approximately KRW 23.24216 trillion) in 2026. The market is then expected to expand further to USD 248.679 billion (approximately KRW 37.49333 trillion) in 2027.

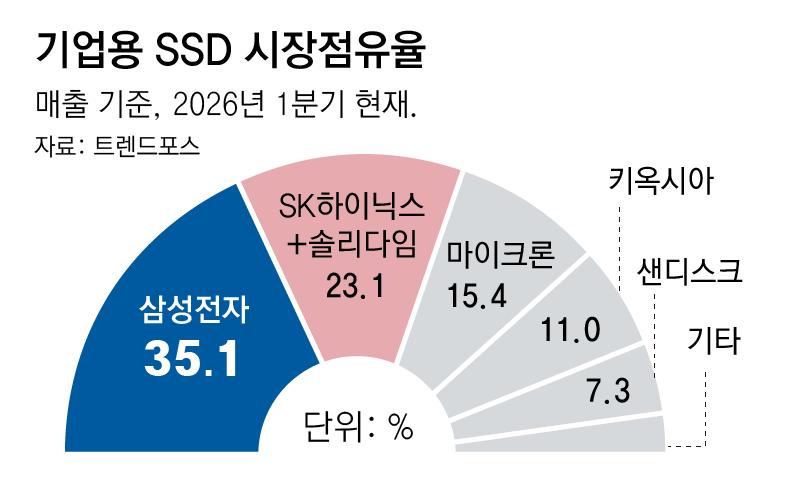

Samsung Electronics currently holds a solid lead in the global eSSD market. According to market research firm TrendForce, in the first quarter of this year (January–March), Samsung ranked first in the global eSSD market with revenue of USD 7.05 billion (approximately KRW 10.6279 trillion) and a 35.1% market share. Its revenue increased 92.8% quarter-on-quarter, far outpacing the market’s average growth rate. SK hynix (including Solidigm) followed in second place with a 23.1% share, and US-based Micron ranked third with 15.4%.

ⓒ dongA.com. All rights reserved. Reproduction, redistribution, or use for AI training prohibited.

Popular News