Amid big tech’s data center expansion race, only a few high‑spec manufacturers see limited gains

Samsung Electro-Mechanics signs KRW 1.5 trillion supply deal

Power equipment also benefits from surging electricity use, coupled with demand to replace aging grids

The tailwind from the artificial intelligence (AI) supercycle is spreading beyond the semiconductor industry to the semiconductor parts sector, which produces capacitors and semiconductor substrates, and to power equipment manufacturers that produce transformers and cables. Securities firms are successively raising their forecasts for these companies’ earnings in the second quarter of this year (April–June). While there is an overflow of demand for AI data center expansion from big tech companies vying to secure products, the number of companies capable of producing high-specification products that meet big tech expectations is limited. Analysts say, as with memory semiconductors, a supplier-dominant market is taking shape.

● Improved earnings outlook for semiconductor component makers

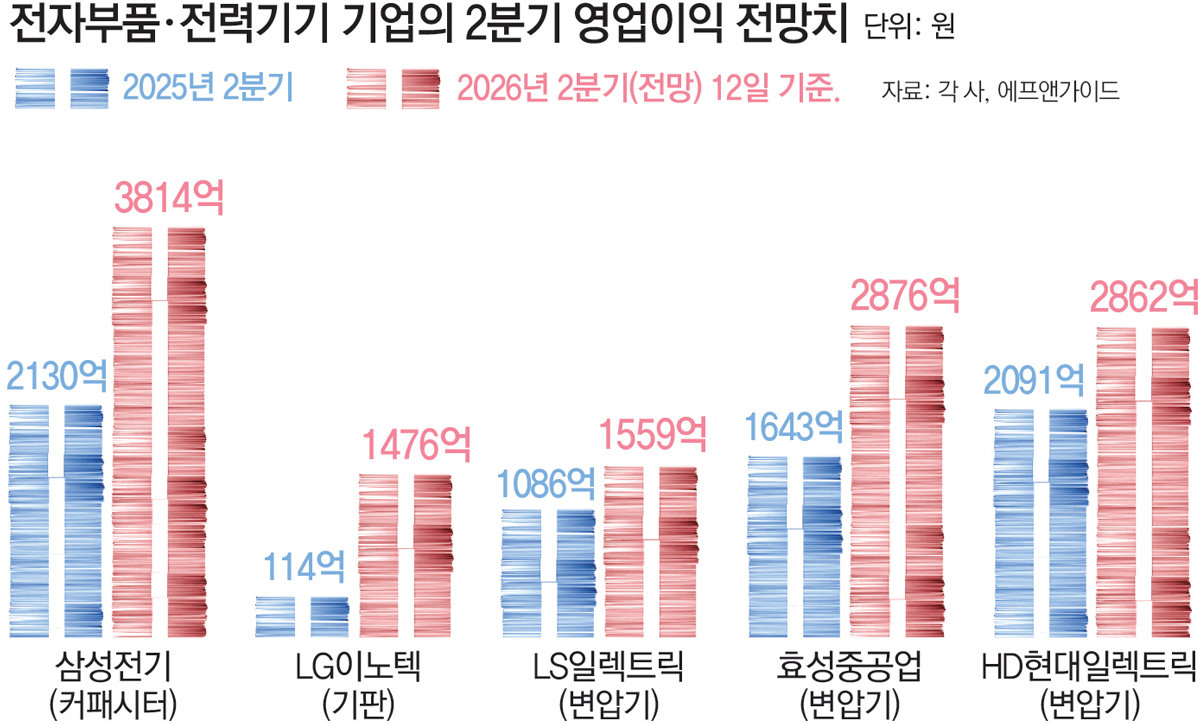

According to financial information provider FnGuide on the 14th, as of the 12th the operating profit forecast for Samsung Electro-Mechanics in the second quarter of this year stood at KRW 381.4 billion. Three months ago, the forecast was KRW 314.7 billion, but ahead of the second-quarter earnings release it has been raised by nearly KRW 70 billion. This outlook is analyzed to be due to strong sales of Samsung Electro-Mechanics’ main product, capacitors. Capacitors are components that act like a “dam,” temporarily storing electricity and supplying power to semiconductors at the right time. A single latest AI server contains about 28,000 multilayer ceramic capacitors (MLCC), and demand for MLCCs is increasing along with the surge in AI data center demand.

In addition, Samsung Electro-Mechanics recently signed a KRW 1.5 trillion supply contract for “silicon capacitors” with a global big tech company. Silicon capacitors are thinner than MLCCs and therefore more suitable for high-performance semiconductors such as high-bandwidth memory (HBM). However, due to high technological barriers and stringent customer certification requirements, the market has been oligopolized by a small number of companies, including Japan’s Murata. In the context of the so-called “Chip War,” where big tech companies are competing to develop their own AI chips, the limited number of suppliers is allowing them to enjoy the benefits of the supercycle.

The second-quarter operating profit forecast for LG Innotek has also risen to KRW 147.6 billion, more than 50% higher than the forecast three months earlier (KRW 98 billion). LG Innotek is attracting attention for its “FC-BGA,” a high value-added semiconductor substrate. Known as a “next-generation substrate,” FC-BGA connects high-performance semiconductor chips to the mainboard and offers faster data processing speeds, lower signal loss, and more efficient heat dissipation than existing substrates. FC-BGA was previously used mainly in PCs, but as big tech firms such as NVIDIA that produce AI chips move to secure substrates, demand has recently surged. As FC-BGA supply shortages have deepened, LG Innotek’s presence in the market has also grown.

● In the AI era, power equipment demand also continues

Earnings expectations are also rising for power equipment manufacturers that produce transformers and cables. This is likewise based on the outlook that the AI supercycle will persist for the time being. The second-quarter operating profit forecasts for Korean power equipment companies such as LS Electric, Hyosung Heavy Industries, and HD Hyundai Electric range between KRW 150 billion and KRW 290 billion, with projections that profits will increase by more than KRW 50 billion–KRW 100 billion year on year. If realized, operating profit would increase by up to about 75% within just one year.

This is analyzed to be because demand for power infrastructure such as ultra-high-voltage transformers and switchgear is rising in tandem with the increase in AI data center demand. In the United States, the largest market for AI infrastructure, electricity consumption is rapidly increasing due to the construction of new AI data centers, but about 70% of the transmission and distribution network is outdated, exacerbating power bottlenecks. As a result, demand for expansion and replacement of power grids is converging, enabling the three Korean power equipment companies to build up order backlogs and secure dominance in the market.

The industry expects the boom for Korean power equipment manufacturers to continue at least until 2030. The Electric Power Research Institute (EPRI) in the United States projected that “the share of data centers in total U.S. power consumption, currently around 4–5%, could surge to 9–17% by 2030.”

ⓒ dongA.com. All rights reserved. Reproduction, redistribution, or use for AI training prohibited.

Popular News