SK Group is accelerating the sale of “core assets” to improve its financial structure and support its battery subsidiaries. Following the recent sale of its renewable energy business unit, the group is now considering transferring its controlling stake in Korea Oil Pipeline Corporation, which generates stable annual operating profit of more than KRW 50 billion, to a domestic private equity fund (PEF). While the group’s aggressive rebalancing drive is gaining momentum, concerns are being raised over the disposal of stable revenue sources.

According to the investment banking (IB) industry on the 24th, SK Innovation is pushing to sell its entire 41% stake in Korea Oil Pipeline Corporation to STIC Investments, a domestic PEF manager. The sale price is reportedly being discussed at around KRW 400 billion.

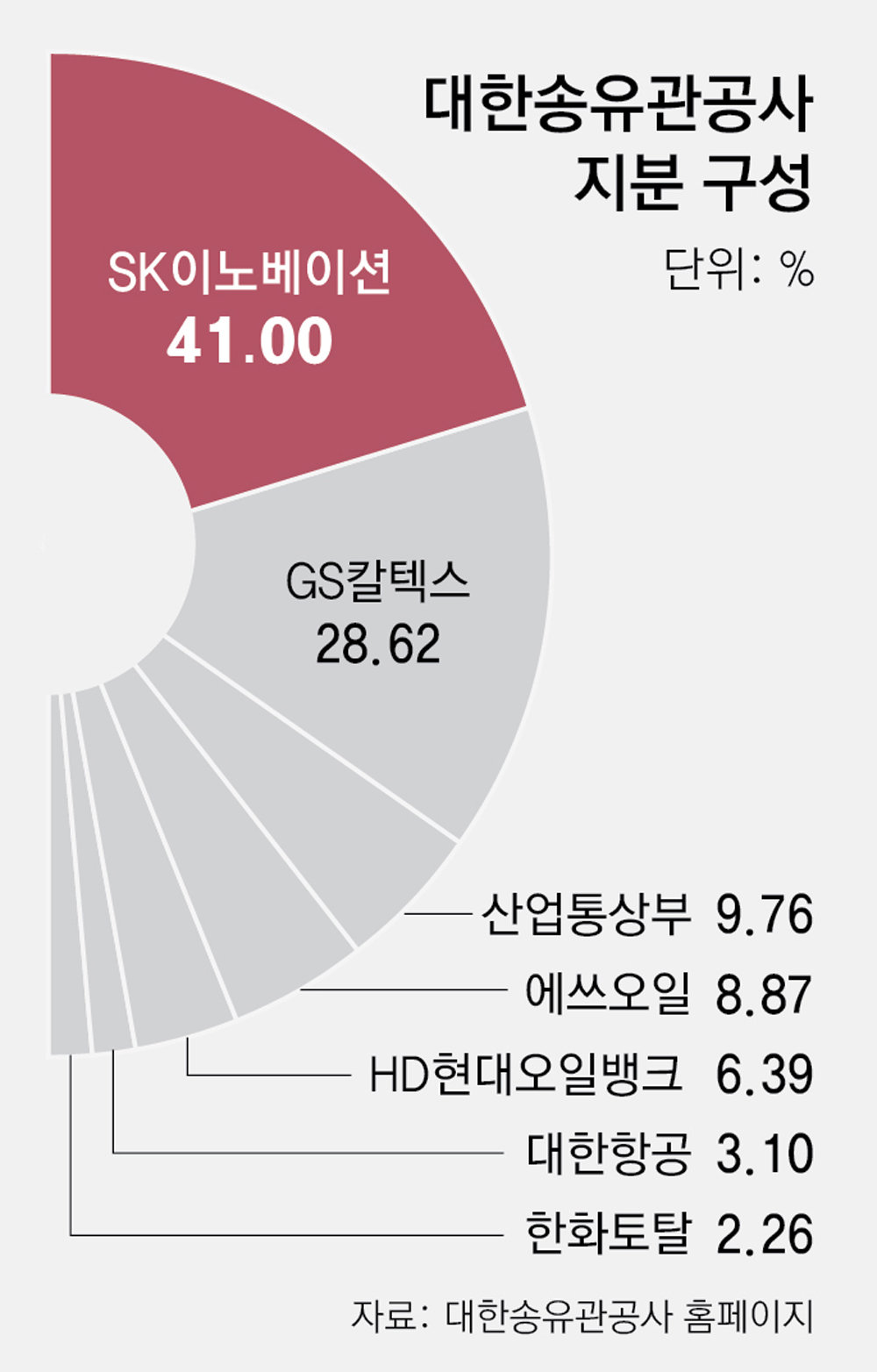

Korea Oil Pipeline Corporation is a domestic energy logistics company that operates and manages pipelines connecting petroleum products produced at refineries to major storage terminals nationwide. SK Innovation secured management control at the time of privatization in 2001 and currently shares ownership with rival refiners GS Caltex (28.62%), S-OIL (8.87%), HD Hyundai Oilbank (6.39%) and the Ministry of Trade, Industry and Energy (9.76%) as major shareholders. SK is said to have initially proposed that existing shareholders acquire its stake, but shifted to an external sale after they declined.

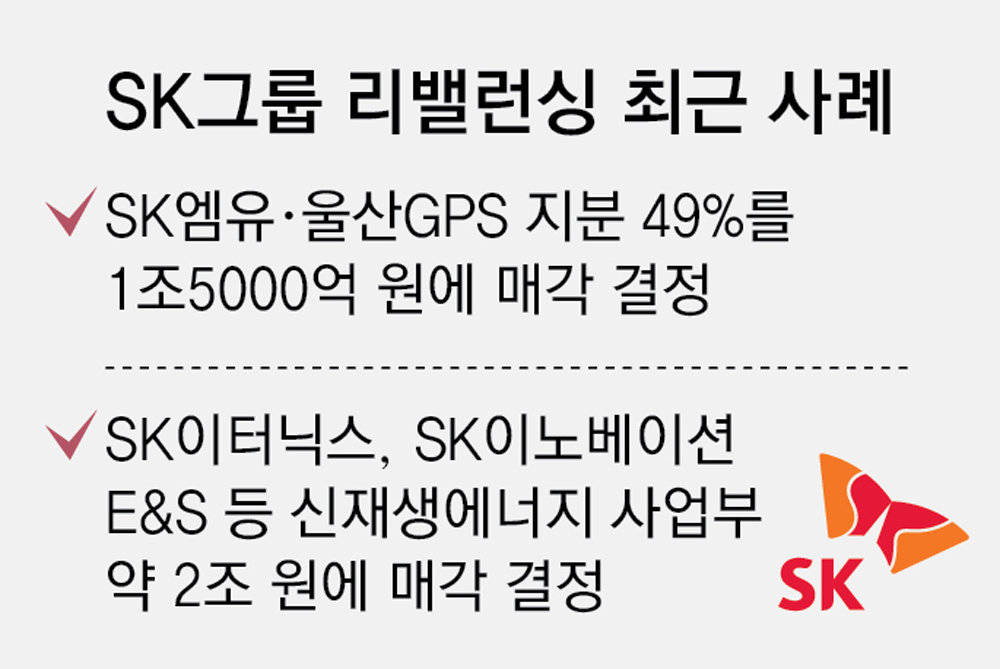

This divestment is seen as an extension of SK Group’s group-wide efforts to “cut excess fat” and “save the battery business.” Last month, it decided to sell a 49% stake in SK MU and Ulsan GPS for more than KRW 1.5 trillion to a consortium of STIC Alternative Asset Management and Korea Investment Private Equity (PE), and also agreed to transfer its renewable energy units, including SK Ethernix and SK Innovation E&S, to global PEF Kohlberg Kravis Roberts (KKR) for about KRW 2 trillion. If the sale of the Korea Oil Pipeline Corporation stake is completed, the group will secure close to KRW 4 trillion in cash from asset sales in the first quarter of this year alone (January–March).

The market is divided between expectations and concerns regarding SK Group’s latest moves. While there is a positive aspect in terms of improving the financial structure by securing liquidity, there are also criticisms that the group’s “core” cash generators are being sold off one after another, raising the risk of undermining profitability.

In fact, Korea Oil Pipeline Corporation is a highly profitable company that recorded KRW 200 billion in revenue and KRW 57.7 billion in operating profit in 2023, and KRW 198.9 billion in revenue and KRW 52.7 billion in operating profit in 2024. On the back of its monopolistic business position, it has generated hundreds of billions of KRW in dividend income every year.

There are also concerns about additional support for the battery subsidiaries. The three major domestic battery makers continue to suffer weak earnings amid the combination of reduced electric vehicle investment by global automakers, a “chasm” (temporary demand stagnation), and low-cost competition from China. With the government itself expressing concern over the competitiveness of the domestic battery industry, there is a risk that large-scale capital injections could turn into “pouring water into a bottomless jar.”

An IB industry source said, “In the case of the Korea Oil Pipeline Corporation stake sale, there are still many hurdles to clear, including the need to persuade shareholders,” adding, “It may take more time before a deal is actually completed.”

ⓒ dongA.com. All rights reserved. Reproduction, redistribution, or use for AI training prohibited.

Popular News