Biopharma

U.S. Advances Pill Diet Drugs, Koreans Left Waiting

Dong-A Ilbo |

Updated 2026.05.09

[Weekly Report] Obesity treatment war enters Round 2 with “oral obesity drugs”

Oral obesity treatments “Wegovy Pill” and “Pfoundeo” to launch in the U.S. this year

Easier dosing and storage than injectables lower the “entry barrier”

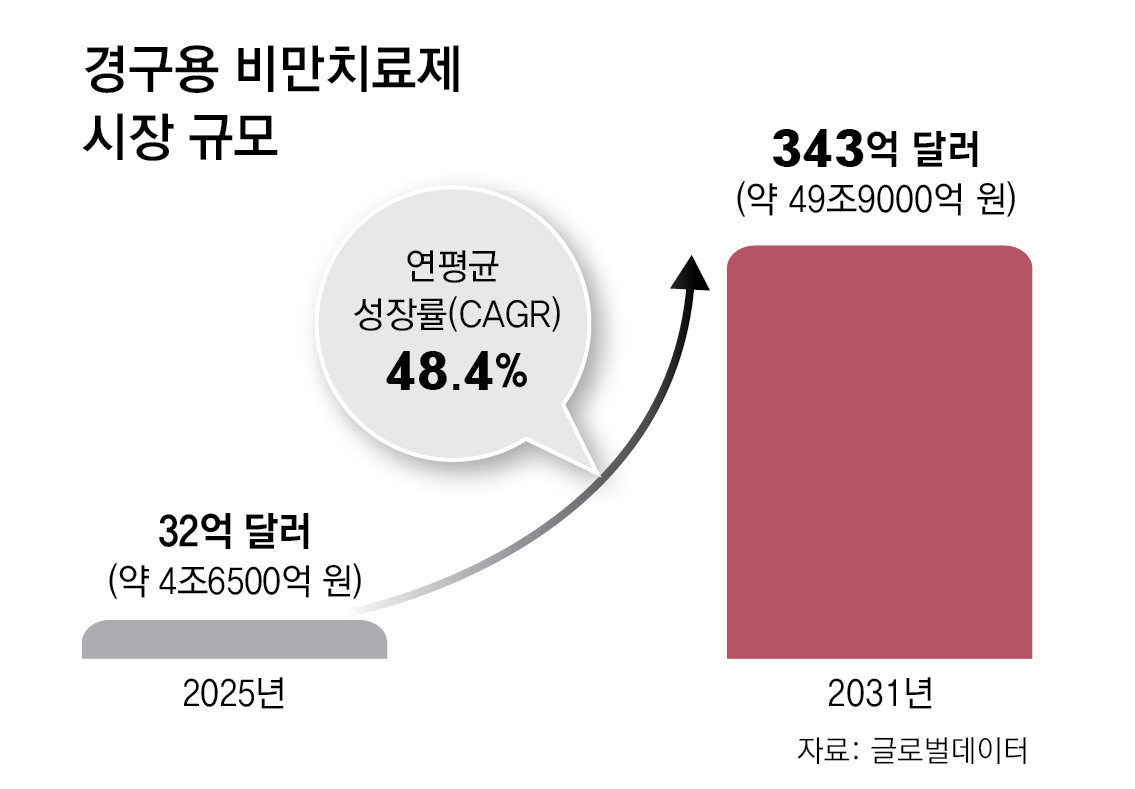

Market projected to reach about KRW 50 trillion by 2031… 10x increase from last year

No application submitted yet to the MFDS… prescriptions in Korea likely from next year or later

Domestic firms including Hanmi Pharmaceutical and Ildong Pharmaceutical accelerate development of “K-obesity drugs”

Oral obesity treatments “Wegovy Pill” and “Pfoundeo” to launch in the U.S. this year

Easier dosing and storage than injectables lower the “entry barrier”

Market projected to reach about KRW 50 trillion by 2031… 10x increase from last year

No application submitted yet to the MFDS… prescriptions in Korea likely from next year or later

Domestic firms including Hanmi Pharmaceutical and Ildong Pharmaceutical accelerate development of “K-obesity drugs”

Getty Images Bank

《Interest in ‘oral obesity drugs’ landing in KoreaIn the United States, the era of ‘oral obesity drugs’ has opened following injectable treatments, transforming not only how people lose weight but also the broader consumption landscape. A flood of small-portion high‑protein foods targeting users of obesity treatments has hit the market, and sales of products designed to alleviate side effects of obesity drugs, such as hair‑loss treatments, are also rising. Korea is one of the hottest markets worldwide for obesity drugs, with the domestic obesity drug market growing 137% year-on-year in 2024. Attention from both industry and consumers is focused on which product will land in Korea first and when: Novo Nordisk’s Wegovy Pill, the world’s first oral obesity drug, or Foundeyo from Eli Lilly, its fast‑follower rival.》

The wish of obesity patients who say they “want to lose weight without needle phobia” is moving closer to reality. Instead of the hassle of injecting themselves with a needle, the era of losing weight with a single pill—“oral obesity drugs”—has fully opened in the US. As competition in obesity treatments enters its second round, attention is also turning to when oral obesity drugs will be launched in Korea.

Glucagon‑like peptide‑1 (GLP‑1) is a hormone secreted from the small intestine after meals that lowers blood glucose and acts on the appetite center in the brain to prolong satiety. Novo Nordisk’s Wegovy and Eli Lilly’s Mounjaro are obesity drugs that mimic this mechanism. Compared with centrally acting psychotropic appetite suppressants, they have significantly fewer side effects and stronger efficacy, sparking a sensation immediately after launch. However, both are injectables that require patients to administer a weekly shot into their abdomen. Fear of needles, the inconvenience of refrigeration, and high prices have been cited as “barriers to entry.”

Initial market reaction has been strong. Novo Nordisk’s Wegovy Pill, which fired the starting signal for oral obesity drugs, received US Food and Drug Administration (FDA) approval in December 2024 and has been sold since this year at more than 70,000 pharmacies across the United States. According to healthcare data analytics firm Truveta, about one‑third (36.1%) of patients prescribed Wegovy Pill in the six weeks after launch were new patients who had never used GLP‑1 drugs before. This indicates that these were newly generated users, not existing obesity‑drug patients switching therapies. Novo Nordisk CEO Maziar Mike Doustdar stated, “The age of the pill has arrived,” adding, “Patients can now achieve weight‑loss effects comparable to injectables with just one pill a day.”

However, even Wegovy Pill, which significantly improves user convenience, has one drawback: it must be taken on an empty stomach and cannot be taken with any beverage other than a small amount of water—stringent administration conditions. For at least 30 minutes after taking the pill, no food or beverages other than water should be consumed to ensure effective absorption. This is because the main ingredient in Wegovy Pill, semaglutide, is a peptide, a group of small amino acids. When peptide drugs are administered orally, their absorption rate in the body is less than 1%, so conditions must be set to maximize absorption. The injectable Wegovy ranges from 0.25 mg to a maximum of 2.4 mg, whereas Wegovy Pill product doses range from 1.5 mg to a maximum of 25 mg.

Source: Companies

Fast‑follower Eli Lilly’s Foundeyo has moved to capitalize on this aspect. Foundeyo’s active ingredient, orforglipron, is a small‑molecule compound rather than a peptide, and thus has relatively higher absorption. As a result, it has differentiated itself in terms of dosing convenience by eliminating requirements such as fasting administration. With the advantage that it can be taken just once, anytime and anywhere, it recorded about 1,400 prescriptions in its first week on the market despite being a latecomer. According to pharmaceutical market research firm IQVIA, Wegovy Pill recorded about 3,000 prescriptions at retail pharmacies in the first four days after launch. While Foundeyo’s initial performance appears somewhat modest by comparison, industry observers say it is too early to draw conclusions given its later launch and the early stage of its rollout.● Fierce race between Novo and Lilly over Korean launch timing

When, then, will these oral obesity drugs arrive in Korea? According to the pharmaceutical industry, as of early this month Wegovy Pill had not yet been submitted for review to Korea’s Ministry of Food and Drug Safety (MFDS). Although the consensus had been that Wegovy Pill, which established a lead in the US market, would also rush to launch in Korea, there is now a view that the Korean rollout schedule may diverge from its global timeline.

Approved by the FDA in December 2024, Wegovy Pill is an oral formulation of the same active ingredient (semaglutide) as the existing injectable Wegovy. By contrast, Eli Lilly’s Foundeyo, approved by the FDA in April, has a different active ingredient from Mounjaro (tirzepatide), the company’s existing injectable obesity drug. The prevailing view had been that Wegovy Pill—based on an already approved ingredient and with earlier FDA approval—would be launched first in Korea as well. However, as both companies are currently still preparing their marketing authorization applications, the industry considers it difficult to predict which drug will reach the market first or to pin down the launch timing.

Some observers even argue that Eli Lilly may have a competitive edge in the race to market in Korea because it included Korean patients in Foundeyo’s global clinical trial (ATTAIN‑1) in 2023. Seven domestic institutions, including Korea University Ansan Hospital, Ajou University Hospital, and Seoul National University Hospital, participated in the trial, meaning Korean patient data have already been secured. With groundwork for domestic approval thus partly in place, once the company decides on the timing of its MFDS filing, the review process could proceed quickly. However, given that new drugs are typically launched 1–2 years after the MFDS filing date, both companies’ obesity drugs are expected to become available for prescription in Korea only from next year at the earliest.

According to IQVIA’s report “2025 Global Obesity Market Landscape,” domestic sales of obesity treatments in Korea reached USD 377 million (about KRW 500 billion) last year, ranking fifth in the world after the United States, Brazil, Canada, and Australia. The growth rate in sales was 137% year-on-year, the highest among the top five countries.

● Korean companies join obesity drug race, entering a ‘Warring States era’?

While the Korean launches of Wegovy Pill and Foundeyo are progressing slowly, domestic companies are accelerating their own obesity drug development efforts. Hanmi Pharmaceutical is the furthest along. In December last year, Hanmi filed an application with the MFDS for domestic approval of its GLP‑1‑class obesity drug candidate efpeglenatide. In a Phase 3 clinical trial involving 448 adults with obesity completed in October 2024, efpeglenatide achieved an average weight loss of 9.75% and a maximum of 30% after 40 weeks of treatment. The company said it applied its proprietary “LAPSCOVERY” platform to efpeglenatide to reduce gastrointestinal side effects, which are considered a major adverse effect of existing obesity drugs. The product is expected to launch as early as the second half of this year (July–December).

IlDong Pharmaceutical, through its new drug development subsidiary Unovia, is developing an oral GLP‑1 therapy, ID110521156. The company has completed Phase 1 trials and in September last year reported results showing an average weight loss of 9.9% and a maximum of 13.8% after once‑daily dosing at the highest dose (200 mg) for four weeks. The company aims to enter global Phase 2 trials this year.

Peptron is developing PT403, a long‑acting GLP‑1 injectable formulated so that a shot currently administered weekly can instead be given once a month. The company explained that its proprietary drug‑delivery platform, “SmartDepot,” is applied to maintain a stable drug concentration.

In a report released last month, IQVIA stated, “This year will be an inflection point that determines the future of the obesity problem due to market acceleration and the launch of new products,” adding, “The current duopoly in the (obesity drug) market (Novo Nordisk and Eli Lilly) will break down as multiple major pharmaceutical companies engage in fierce competition.”

Jeon Hye-jin; Choi Ji-won; Kim Jae-hyung

AI-translated with ChatGPT. Provided as is; original Korean text prevails.

ⓒ dongA.com. All rights reserved. Reproduction, redistribution, or use for AI training prohibited.

Popular News