Ola Fintech expands working capital access for microbusinesses

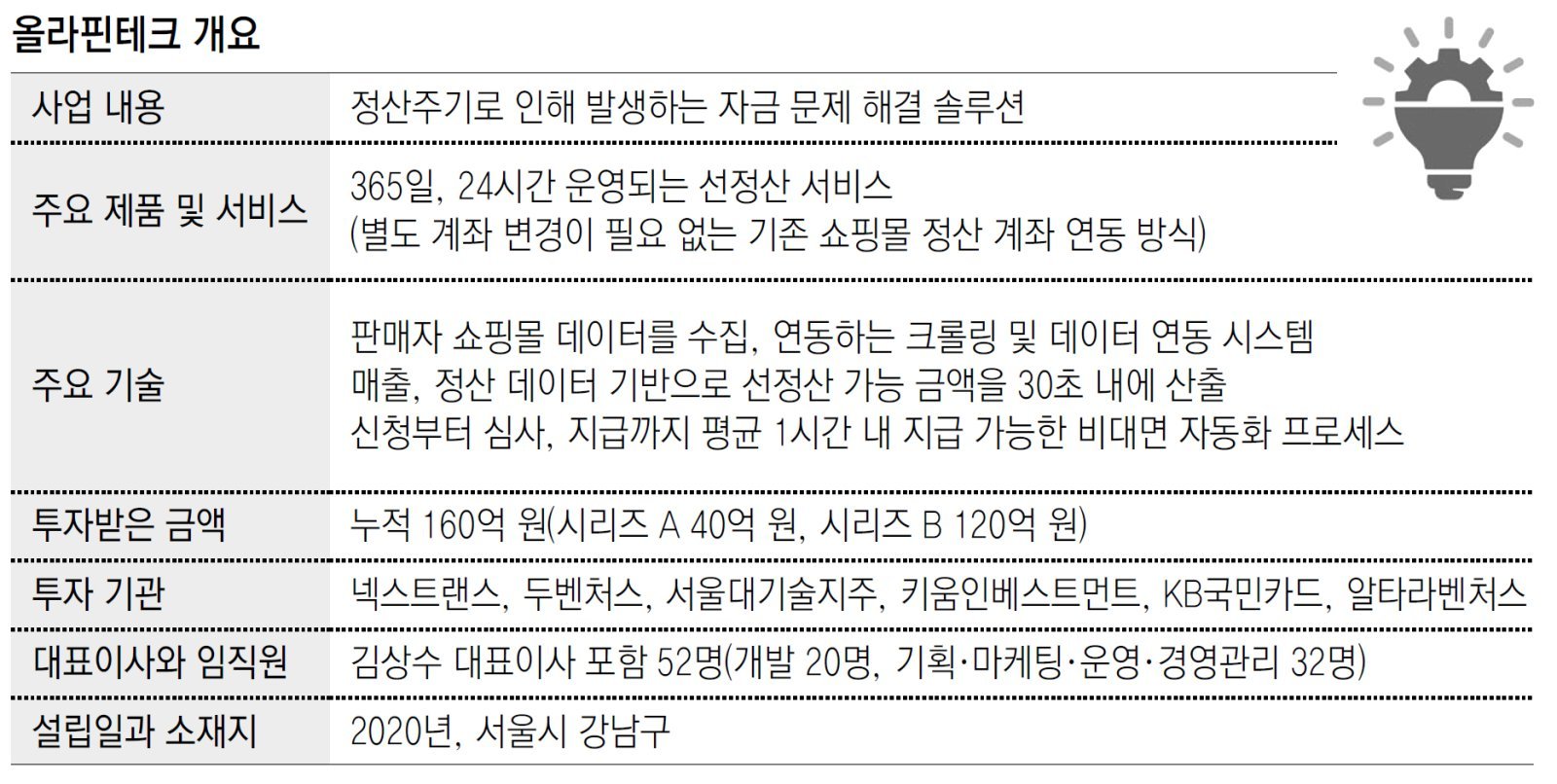

Pre-settlement payouts within an hour using an evaluation engine for merchants who normally wait 1 week–2 months

Targets small firms without bank loan access, assessing over 200 indicators including sales and operational capacity

Three co-founders devoted 10 months of full-time preparation, turned profitable last year… “Financial support for all business owners”

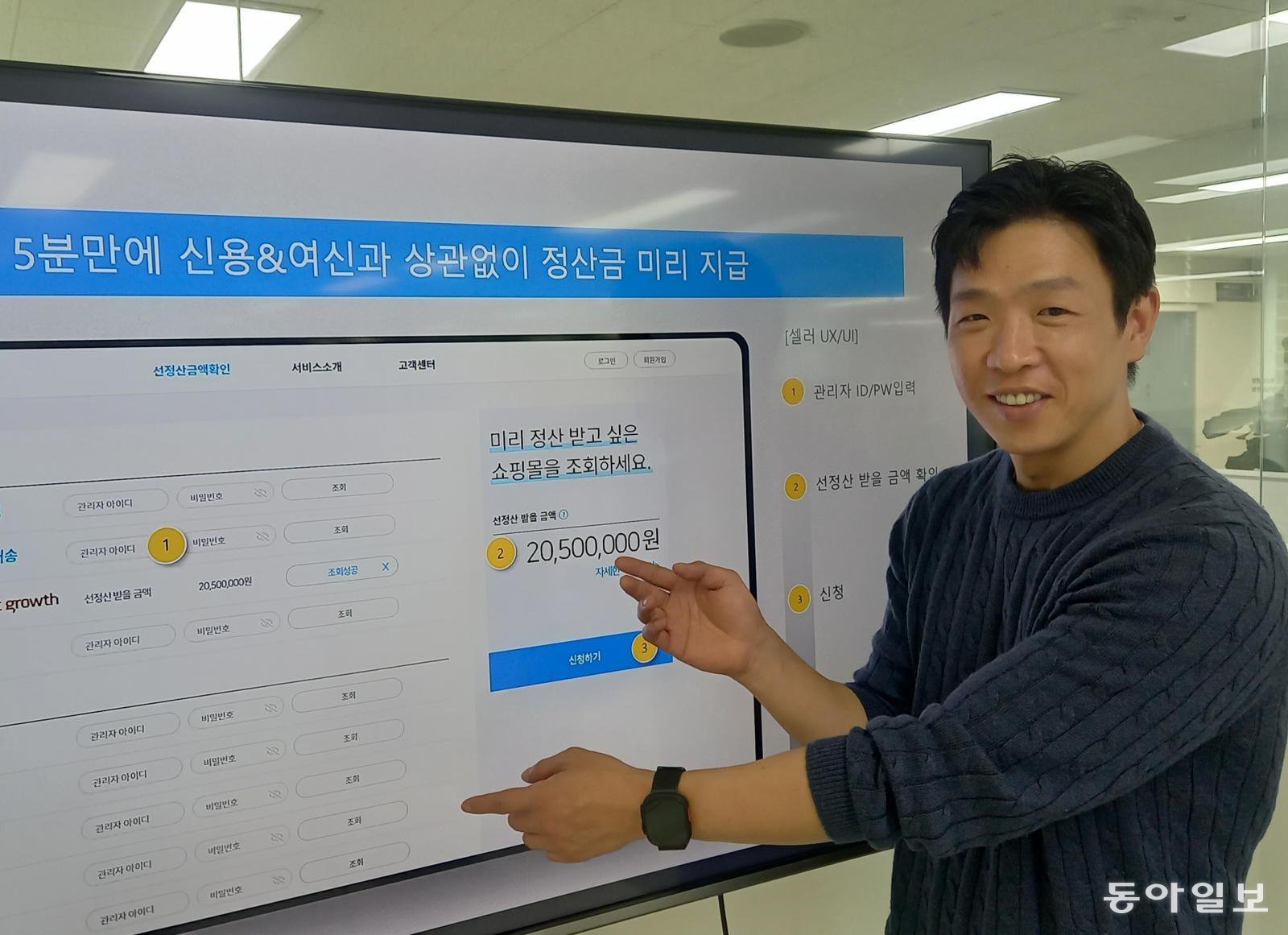

On April 2, Ola Fintech CEO Kim Sang-su explains how the company’s service is implemented, using the example of a seller operating in an online shopping mall, at the company’s office in Gangnam District, Seoul. Photo by reporter Heo Jin-seok, jameshur@donga.com

There is a boss who runs a kalguksu (knife-cut noodle) restaurant. This owner-operator faithfully sells 200 bowls a day. Payments to the flour supplier go out on the 5th of every month, and part-time workers’ wages are paid on the 15th. But today is the 4th. The bank account balance has hit rock bottom. Once the full month’s cycle is complete, the business is profitable, but at this very moment, the owner is desperately short of KRW 2 million.

What options are available in such a situation? Banks do not lend to the kalguksu restaurant owner, who has no financial statements and insufficient credit data. The owner goes to the neighboring shopkeeper. “Mr. Kim, could you lend me KRW 2 million? I’ll pay you back KRW 2.2 million next month.” If that does not work, the owner takes out a high-interest loan using a life insurance policy as collateral.

Such situations are far from unfamiliar to the hundreds of thousands of microbusiness owners and small entrepreneurs nationwide. The volume of funds that small merchants borrow from private lenders for working capital and other needs amounts to KRW 45 trillion annually. When Ola Fintech CEO Kim Sang-su (47) first encountered this figure, it sparked the idea of starting a business in his mind. Meeting at Ola Fintech’s office in Gangnam District, Seoul, on April 2, Kim said, “I thought that if this problem could be solved, it would be socially meaningful as well. The market size of KRW 45 trillion also served as a stimulus for launching a startup.”

● ‘Capital hell’ swallowing small merchants The reason small merchants are denied bank loans is not because they are “bad” borrowers. It is because there is no data available for financial institutions to determine that they are not bad borrowers. When assessing an individual, a vast amount of information such as salary history, auto installment records, and whether the person rents or owns a home flows into financial institutions. But when a small merchant walks in with nothing more than a simplified-taxpayer business registration number, the bank’s response is always the same: “Bring your financial statements.” For example, even if someone has diligently sold, delivered, and packaged goods for three years, without organized financial statements that person effectively does not exist within the financial system.

According to the Korea Small Enterprise and Market Service, as of 2022, private loans accounted for 34.4% of new funding raised by self-employed individuals. Outstanding high-interest loans exceeded KRW 43.6 trillion. The proportion of business operators who have experienced having their loan applications rejected by financial institutions stands at 49%.

Kim said, “Finance should play a positive role of helping when times are tough and getting repaid when times are better, but in modern society, finance is like taking away the umbrella when it rains and offering it when the sun is shining. The reason small merchants are constantly struggling with capital shortages is not their fault; it is because financial institutions are structurally lacking the factors needed to assess them.”

● “Funds will be deposited within an average of one hour” Ola Fintech’s solution is simple yet innovative. When an online seller assigns to Ola Fintech the “settlement receivables” that will be paid by platforms such as Coupang or Gmarket, Ola Fintech uses artificial intelligence (AI) to instantly evaluate real-time sales data and advances cash. Because this is a purchase of receivables rather than a loan, it leaves no trace on the seller’s credit rating.

What made this service a true innovation was its structural design rather than the technology itself. At the time the service was launched, competitors required users to change their settlement account to the competitor’s account or submit piles of paperwork. It felt like going to a bank to apply for a loan.

Ola eliminated all of that. While keeping the existing shopping mall settlement account as it is, the company processes everything from application to assessment and payment through non-face-to-face automation and deposits the funds within an average of one hour. Kim said, “Previously there were no firms offering this level of convenience. Five to six years on, competitors have benchmarked us and become similar. This is a change that we created.”

Naturally, there are fees. Kim said, “Settlement cycles differ by shopping mall, so the fees also vary, from 0.4% to 2.0%. If you receive KRW 10 million as an advance at a fee of 1% per transaction, the fee comes to KRW 100,000. It is true that we are giving business operators a choice for arranging funds, but we also incur costs to raise capital, so in annualized terms the rate is around the mid-range (below 15%). That is why we advise using it only for short-term working capital needs.”

Ola Fintech’s core technology is its proprietary “non-financial credit assessment model.” It collects sales and settlement data in real time and calculates the amount eligible for advance payment within 30 seconds. It automatically computes a business operator’s reliability score by combining around 200 elements, including quantitative indicators such as sales volume and cancellation rate, and qualitative data such as customer reviews and customer service (CS) response speed. At present, it supports integration with more than 20 shopping malls, the highest level domestically, and operates 24 hours a day, 365 days a year.

● Thoughts and actions behind the decision to start a business It appears that what enabled Kim to move beyond a simple idea and actually launch a startup was a clear-eyed self-awareness. Born in 1979, he took his first step into the workforce in 2006 and gained direct experience at the intersection of payments, commerce, and finance through roles at Hannet (ATM/PG), KSNET (PG Business Team), SK Planet (Finance Support Team Manager), and Danal (Head of Card Business Team). Over 14 years of delving into the essence of the industry, he reached one conviction: that he could resolve the challenges in this sector, which he understood so well, with his own knowledge and capabilities.

The very first thing he did before founding the company was to look for co-founders. The people he turned to were Vice CEO Jeong Nam-gi-hyeon, whom he had met at Danal, and current Growth Division Head Ko Kyung-hwan. Vice CEO Jeong is a business planning expert who worked at Com2uS, LG Uplus, and Sega Publishing Korea before serving as Head of External Strategy at Danal, while Growth Division Head Ko is a former art director who has led branding and product-making initiatives. Kim said, “I recommend co-founding rather than starting a business alone. Dividing work according to each person’s capabilities and roles, and sharing the same dream and working toward it together, provides far more strength than one might expect.”

In January 2019, the three of them committed themselves full-time to preparing the startup. For more than 10 months, they engaged in intense discussions, researched the market, and verified the numbers. Kim said, “We did not just discuss how much profit we could make or whether the business would be sustainable. We also asked how much this business, if successful, could make our hearts race—that was also subject to consensus among us.” Through this process, he said, he came to feel that he was someone who could run a business. “Even if things did not go well, I am not the type to destroy myself. I was firmly resolved that, if necessary, I could do delivery work or something else and start again.”

What keeps a founder going to the end is not the business plan, but an inner answer to the question, “Why must this work be done?” For Kim, that answer lay in the figure of KRW 45 trillion. “If this problem is solved, that KRW 45 trillion currently mobilized through private loans can be raised in some form from financial companies instead. Then interest rates will fall and people will be able to run their businesses in much better conditions,” he said.

● Evolving into a service for all business operators

Ola Fintech participating in the 2025 Korea E-commerce Fair. Provided by Ola Fintech

As of February this year, Ola Fintech’s cumulative payout amount stood at KRW 6.8078 trillion, with a cumulative 1,023,432 payouts and 41,383 cumulative subscribers. Each month, 4,000–5,000 business operators are securitizing KRW 90–100 billion. Ola Fintech currently supports this scale by attracting capital from KB Kookmin Card and Kiwoom Capital.

After launching its service in 2020 with annual revenue of KRW 100 million, the company’s revenue grew to KRW 3.6 billion in 2022, KRW 9.5 billion in 2023, and KRW 17 billion in 2024. In 2025, it recorded its first net profit, posting revenue of KRW 20.5 billion and net income of KRW 700 million. The business is not without risk, the biggest of which is non-performing receivables. “A single non-performing receivable can eat away the profit from 100 successful cases. We must overcome this through economies of scale based on our evaluation engine,” Kim said.

Ola Fintech began making major strides this year. In February, it launched “REVN,” a service that applies the advance-settlement model to all business-to-business (B2B) operators with confirmed sales receivables, extending beyond e-commerce. Its medium- to long-term roadmap is more ambitious. The company plans to reach KRW 50 trillion in data-based business loans by 2027–2028 and to become a global player based in Southeast Asia from 2029 onward.

“We currently provide around KRW 3 trillion in liquidity per year, which is not even one-tenth of the KRW 45 trillion. There are far more business operators facing difficulties,” Kim said. “We want to steadily realize our vision of ‘solving the funding problems of all business operators.’”

ⓒ dongA.com. All rights reserved. Reproduction, redistribution, or use for AI training prohibited.

Popular News