Korea’s position in the global electric vehicle (EV) battery market is being squeezed by China. Even in the global market excluding China’s domestic demand, Korean batteries are losing market share while Chinese companies are consolidating control. In response, the domestic battery industry is seeking ways to survive through so-called “value shift,” overhauling a business structure that has been heavily concentrated in EVs toward higher-growth sectors such as energy storage systems (ESS) and humanoid robot batteries.

● Global gap widens due to divergent paths between NCM and LFP

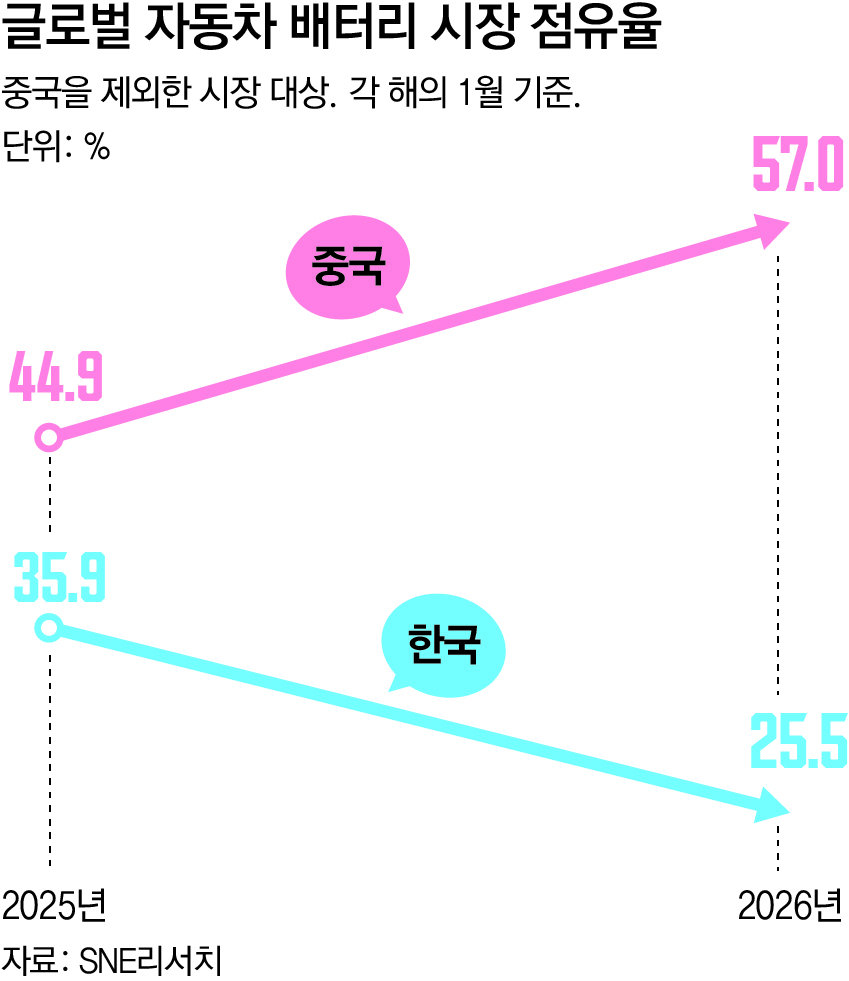

According to market research firm SNE Research, global (excluding China) EV battery usage in January this year reached 32.7 GWh (gigawatt-hours), up 13.7% year-on-year. Despite the EV “chasm” phase of temporary demand stagnation, the market continued to post double-digit growth. However, the combined market share of Korea’s three major battery makers (LG Energy Solution, SK On, Samsung SDI) was only 25.5%, down 10.4 percentage points from 35.9% a year earlier.

In contrast, Chinese companies are rapidly expanding their share. CATL recorded 11.2 GWh, up 26.5% year-on-year, for a market share of 34.2%, surpassing the combined share of the three Korean companies and maintaining its No. 1 position. This reflects its expansion of supply chains to global automakers such as Volkswagen and Audi. BYD also rose to third place after LG Energy Solution, supported by the expansion of its sales network in Europe and emerging markets.

The decline in market share of the Korean battery industry is seen as the result of both strategic differences in cathode technology and China’s large-scale industrial support policies. In the early days of commercialization, Korea focused its capabilities on nickel-cobalt-manganese (NCM)-based “ternary batteries,” which have high energy density and long driving range per charge. China, by contrast, concentrated on advancing lithium iron phosphate (LFP) technology, which is heavier and offers a shorter driving range but has lower production costs.

Initially, driving range was the primary competitive factor, but market conditions have gradually changed. As global inflation persisted and EV subsidies were reduced, price competition among automakers intensified, prompting a rapid increase in the adoption of cost-effective LFP batteries to cut production costs. Advances in packaging technologies such as Cell to Pack (CTP) have also helped mitigate LFP’s chronic weakness of low energy density, accelerating its adoption.

According to SNE Research statistics, LFP’s share based on cathode material loading, which was only 34% in 2021, has steadily risen and is projected to reach 62% in 2025, establishing itself as the market mainstream. In contrast, the share of ternary batteries, which stood at 66% in 2021, is expected to shrink to 38% by 2025.

● KRW 320 trillion-scale industrial support in China

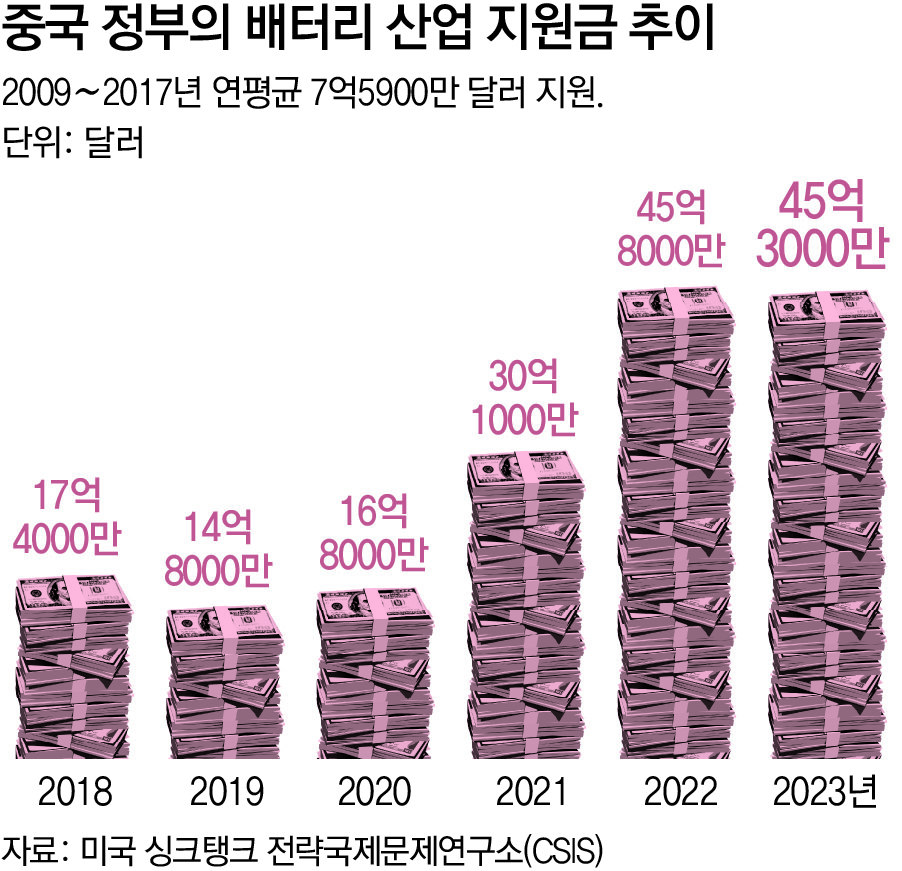

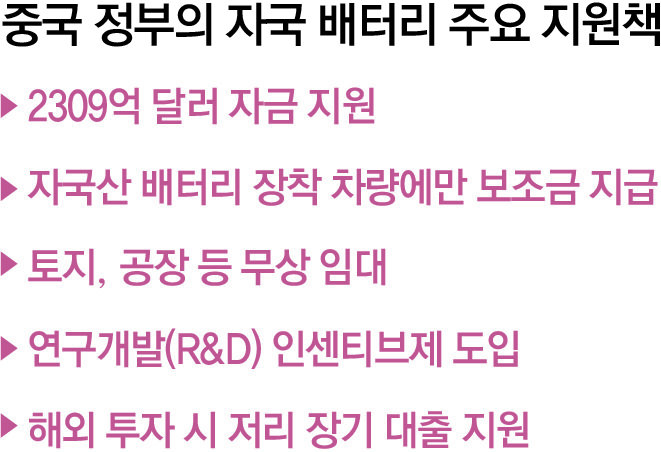

The rapid advance of Chinese companies in LFP technology and their expanded market share are underpinned by extensive financial support from the Chinese government. The Center for Strategic and International Studies (CSIS) in the United States estimates that the Chinese government injected a total of USD 230.9 billion (about KRW 320 trillion) into the battery and EV industries from 2009 to 2023. This figure includes only quantifiable items such as buyer rebates, sales tax exemptions, and research and development (R&D) support; the actual amount is considered much larger when adding land grants, electricity subsidies, and other support measures.

In 2012, China announced its “Energy-Saving and New Energy Vehicle Industry Development Plan,” designating EVs as a national strategic industry. In 2015, it introduced the so-called “white list” system, under which subsidies were preferentially allocated only to EVs equipped with batteries made by domestic manufacturers, thereby protecting its domestic industry.

It also introduced large-scale incentive schemes. Local governments built plants and leased them free of charge, and allowed land to be used at no cost. They subsidized 20–40% of total capital expenditures (CAPEX), and in some cases allowed pre-tax R&D expenses to be additionally deducted by up to 100–200%. For overseas investments, companies could receive low-interest loans at around 2% with maturities of 15–20 years from the Export-Import Bank of China.

The volume of support continued to grow even after the industrial ecosystem had taken root. CSIS data show that annual support, which averaged less than USD 1 billion between 2009 and 2017, increased to an annual average of USD 1.64 billion from 2018 to 2020, and expanded further to more than USD 4 billion annually from 2021 to 2023. Market leader CATL alone received USD 1.8 billion in government subsidies between 2018 and 2023. In addition, China has a high degree of self-sufficiency in major mineral supplies that serve as raw materials, while Korea relies on overseas sources for 70–90% of key materials such as precursors and lithium. Given this, and China’s massive domestic market, it is difficult for Korean companies to match Chinese rivals in price competitiveness and production scale.

● Diversification into ESS battery business

The domestic battery industry is at a critical juncture for survival. It faces the task of avoiding the fate of chemicals, steel, and displays, which ceded leadership under the pressure of China’s vast domestic demand and subsidies, and instead following the path of semiconductors, automobiles, and shipbuilding, which lead the market through overwhelming technological competitiveness and the pioneering of new markets. To this end, battery makers are seeking breakthroughs through proactive diversification of their business structures.

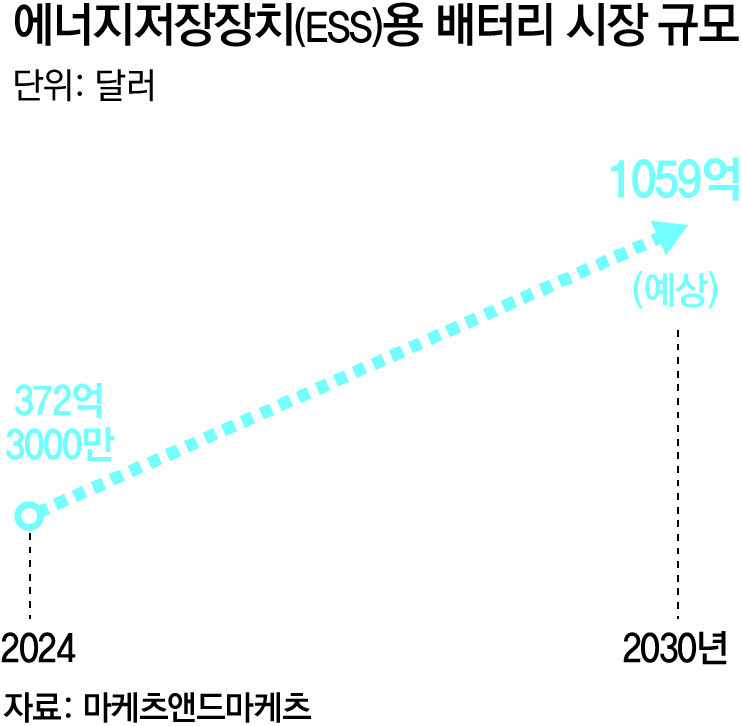

The ESS market, where power demand is rising alongside the expansion of artificial intelligence (AI) data centers, is emerging as the first major alternative. Big Tech companies are rapidly increasing investment in AI data centers, but it typically takes 7–11 years to connect to existing power grids and build transmission infrastructure. To shorten this timeline, a growing number of operators are installing power facilities directly on data center sites. In this process, large-scale ESS integration has become essential to balance power supply and demand. The global ESS market is projected to grow steadily from USD 37.23 billion (about KRW 55 trillion) in 2024 to USD 105.9 billion (about KRW 155 trillion, forecast) in 2030.

Korean battery manufacturers are aggressively targeting the North American ESS market, where entry by Chinese firms is constrained by U.S. government restrictions. Market observers expect the market share of Korean battery makers, previously in the 10% range, to rise to as much as 30%.

LG Energy Solution has preemptively secured a large-scale LFP ESS production system in North America through its Michigan plant, the NextStar Energy plant in Canada, and its joint venture with Honda. On this basis, it signed a KRW 6 trillion ESS battery supply contract with Tesla last year. Samsung SDI, leveraging its strength in non-Chinese prismatic batteries, won a KRW 2 trillion battery supply contract with a U.S. energy infrastructure company last year, and this month signed an additional contract worth about KRW 1.5 trillion with a major U.S. energy company. SK On also entered the large-scale North American ESS market in earnest by signing a KRW 2 trillion battery supply agreement last year with Flatiron, a U.S. renewable energy developer.

● Humanoid robot market favors high-density ternary batteries

The industry is also eyeing the “humanoid robot market,” a future sector that demands high-density battery technology. Humanoid robots, which must operate in the same environments as humans, need to house their power sources within limited body structures and narrow joints. Due to these spatial constraints, the energy density per unit weight of battery cells becomes a key metric that determines the robots’ operating time and performance.

In this field, heavy, iron-based LFP batteries with comparatively low energy density (an average of 90–170 Wh per kg) are less likely to be adopted. By contrast, ternary batteries, a segment led by Korean manufacturers, can achieve high energy density of 200–300 Wh per kg on average. They are regarded as an optimal technology for the robotics industry, which must minimize volume while maximizing output. In terms of average voltage, LFP (3.2 V) also falls below ternary batteries (3.6–3.8 V), posing physical limits to capacity expansion.

Domestic companies are accelerating efforts to build a battery ecosystem for robots. They are supplying high-nickel 2170 cylindrical batteries on a priority basis to major robot manufacturers to accumulate data, while focusing R&D on the next-generation “anode-free all-solid-state battery,” with a commercialization target of 2030. The anode-free approach, which uses only a current collector without an anode material, replaces flammable liquid electrolytes with solid ones, reducing fire risk and dramatically increasing theoretical energy density. It is expected to become the standard in next-generation mobility and robotics.

An industry insider in the battery sector said, “Portfolio diversification strategies, such as expanding into the North American ESS market and preempting the next-generation robot market, are likely to be key variables for improving the mid- to long-term performance of the domestic battery industry and defending its market share.”

ⓒ dongA.com. All rights reserved. Reproduction, redistribution, or use for AI training prohibited.

Popular News